Call now to get maximum compensation

for your auto accident injuries.

One Of Hawaii's

Top Auto Accident

Attorneys

Worked for U.S. Air Force JAG

Millions obtained for our Clients' Car Accident Injuries

No Fees Until We Win Your Auto Accident Case

Lowest Fees Guaranteed

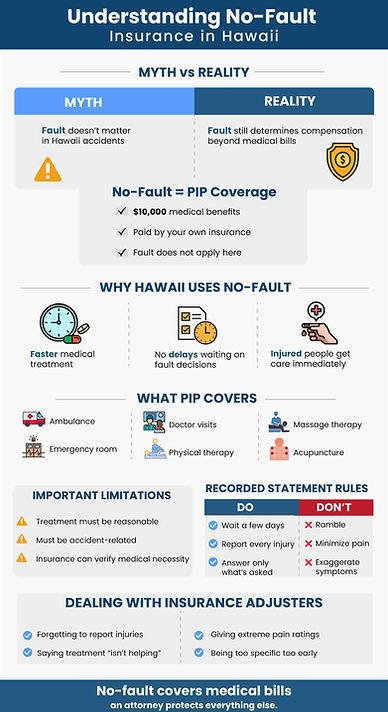

No-Fault Insurance In Hawaii

Hawaii is referred to as a “No-Fault State,” and that phrase often creates serious confusion for drivers who have been involved in a motor vehicle accident. Many people believe that if they are injured in a crash in Hawaii, fault simply does not matter. We regularly receive calls from individuals who assume that because Hawaii is a no-fault state, no one can be held legally responsible for causing the accident.

That assumption is incorrect.

Understanding how no-fault insurance works in Hawaii is critical to protecting your rights after a crash. While no-fault insurance provides immediate medical benefits, fault absolutely still matters when it comes to recovering full compensation for your injuries.

What Does “No-Fault” Actually Mean in Hawaii?

In Hawaii, no-fault insurance refers to Personal Injury Protection (PIP) coverage. By law, every auto insurance policy issued in Hawaii must include at least $10,000 in PIP medical benefits.

These benefits apply regardless of who caused the accident.

However, this does not mean fault is irrelevant. Fault still determines whether you can pursue compensation beyond the initial $10,000 in medical benefits, including:

-

Pain and suffering

-

Emotional distress

-

Lost wages

-

Future medical care

-

Permanent disability

-

Loss of enjoyment of life

As a leading Hawaii Auto Accident Injury Lawyer, David W. Barlow regularly helps injured victims understand the distinction between PIP benefits and full injury claims against at-fault drivers.

Why Hawaii Uses a No-Fault System

The purpose of Hawaii’s no-fault law is to ensure that injured people receive immediate medical care without delay. After a crash, it can take weeks or even months for insurance companies to determine who is legally responsible. The legislature designed the system so accident victims do not have to wait for fault investigations before receiving treatment.

Under Hawaii law:

-

The insurance covering the vehicle you were in pays the first $10,000 in medical expenses.

-

This applies whether you were the driver, passenger, or even a pedestrian struck by the vehicle.

-

Payment is made without regard to fault.

Many people are surprised to learn that their own insurance company must initially pay their medical bills — even if another driver clearly caused the crash. But the law prioritizes immediate treatment and recovery over fault disputes.

What Does Hawaii No-Fault Insurance Cover?

Hawaii PIP coverage pays for reasonable and necessary medical treatment related to accident injuries. This typically includes:

-

Ambulance transportation

-

Emergency room care

-

Hospital treatment

-

Diagnostic imaging (X-rays, MRIs, CT scans)

-

Doctor visits

-

Physical therapy

-

Chiropractic care

-

Massage therapy

-

Acupuncture

-

Prescription medications

-

Certain rehabilitation services

If the treatment is related to injuries caused by the accident and is considered medically necessary, it may be covered under PIP — up to the $10,000 limit.

An experienced Hawaii Auto Accident Injury lawyer like David W. Barlow can help ensure your medical treatment is properly documented and submitted to maximize your available benefits.

When Fault Still Matters in Hawaii

Although PIP pays initial medical bills, you may step outside the no-fault system and pursue a claim against the at-fault driver if:

-

Your medical bills exceed $5,000; or

-

You suffer permanent injury, significant disfigurement, or serious impairment.

-

In these cases, fault becomes extremely important. Once you cross the “tort threshold,” you may seek compensation for:

-

Pain and suffering

-

Full wage loss

-

Loss of earning capacity

-

Long-term care needs

This is where hiring a knowledgeable Hawaii Injury Lawyer becomes critical. David W. Barlow and his team work to hold negligent drivers accountable and pursue full compensation beyond basic PIP benefits.

Insurance Companies Still Scrutinize Your Claim

Even though no-fault benefits are automatic, insurance companies do not simply approve every bill without review. They are only required to pay for treatment that is:

-

Reasonable

-

Necessary

-

Accident-related

Insurance adjusters carefully review medical records and may question whether your injuries were pre-existing or caused by something other than the accident.

Remember: adjusters work for the insurance company — not for you.

As David W. Barlow often advises clients, it is important to approach communications with insurers carefully and strategically.

The Recorded Statement – Proceed With Caution

Shortly after the accident, your insurance company will likely request a recorded statement. This is a formal interview about:

-

How the accident occurred

-

What injuries did you sustained

-

Whether you had prior medical issues

We generally recommend waiting several days before giving this statement. Some injuries, particularly soft tissue injuries and concussions, may not appear immediately. Adrenaline can mask pain, and symptoms often develop later.

When giving a recorded statement:

-

Report every injury, even minor ones.

-

Be truthful and accurate.

-

Do not guess or speculate.

-

Answer only the question asked.

If you fail to report an injury initially, the insurer may later deny coverage for treatment related to that injury.

For example, if you state that only your upper back hurts but later develop lower back pain, the insurance company may argue the lower back injury is unrelated.

An experienced Hawaii Auto Accident Injury Lawyer like David W. Barlow can help you prepare for this process and protect you from common pitfalls.

Completing the No-Fault Application

In addition to a recorded statement, you will need to complete a written application for PIP benefits. This form requires you to describe:

-

Your injuries

-

Medical providers

-

Employment information

-

Accident details

When completing the application:

-

Include all symptoms.

-

Be thorough but accurate.

-

Avoid minimizing your injuries.

If unsure, it is often better to describe injuries broadly (for example, “back pain” rather than specifying only one region).

Be Aware of Insurance Company Tactics

Insurance adjusters are trained professionals. They may appear friendly and helpful, but their job is to protect the company’s financial interests.

Common strategies include:

-

Looking for prior injuries to blame your symptoms on

-

Asking you to rate your pain on a 1–10 scale

-

Suggesting treatment is unnecessary

-

Requesting an Independent Medical Examination (IME)

If you rate your pain too low, they may argue that you do not need treatment. If you rate it too high, they may claim you are exaggerating.

Balance and accuracy are key.

As a trusted Hawaii Auto Accident Injury Lawyer, David W. Barlow helps clients navigate these tactics and ensures that legitimate injuries are taken seriously.

Independent Medical Examinations (IMEs)

In some cases, the insurance company may require you to attend an IME with a doctor they select. These exams are often used to determine whether ongoing treatment is “necessary.”

It is important to understand that:

-

The IME doctor is hired by the insurance company.

-

Their opinion may impact whether future treatment is approved.

Before attending an IME, it is wise to understand your rights and consult with legal counsel.

Peace of Mind After a Hawaii Auto Accident

The purpose of Hawaii’s no-fault system is to provide peace of mind. If you are injured in a car accident in Honolulu or anywhere in the state, you can seek immediate medical care without waiting for fault determinations.

However, PIP benefits are only the beginning.

If another driver caused your injuries, you may be entitled to significantly more compensation than the initial $10,000 in medical coverage. Holding negligent drivers accountable helps ensure you are fully compensated for:

-

Physical pain

-

Emotional suffering

-

Lost income

-

Long-term medical needs

David W. Barlow has helped countless injury victims throughout Hawaii understand their rights and pursue the compensation they deserve.

Protect Your Rights After a Hawaii Car Accident

Navigating Hawaii’s no-fault insurance system can be complicated. While the system is designed to provide fast medical coverage, insurance companies still actively work to limit payouts.

Your goals should be:

-

Obtain appropriate medical treatment.

-

Accurately document all injuries.

-

Avoid statements that could undermine your claim.

-

Understand when you may pursue a claim against the at-fault driver.

If you have questions about no-fault insurance, PIP benefits, or your right to pursue additional compensation, consulting an experienced Hawaii Lawyer can make a significant difference in the outcome of your case.